Circle Stock Is Down 65% From Its High. Here’s Why Circle’s Stablecoin Expansion Could Still Drive Outsized Returns

Key Stats for CRCL Stock

- Past week’s performance: -7.9%

- 52-week range: $50 to $263

- Valuation model target price: $209

- Implied upside: +203.2% over 2.5 years

Run Circle’s valuation for yourself in under 60 seconds with TIKR’s free Valuation Model >>>

Circle’s Payment Network Grows While the Stock Pulls Back

Circle Internet Group (CRCL) dropped roughly 14% over the past week, continuing a sharp selloff from its 52-week high of $263. The stock now trades near $69, which is below its IPO range, but the company’s underlying USDC network has continued to expand. Investors are clearly rethinking the valuation, but the business momentum is pointing in the opposite direction.

The week’s most significant development arrived on June 26, when Nomura announced a strategic partnership with Circle to use USDC for global financial services, including collateral management and fund transfers. Nomura is one of Japan’s largest financial institutions, so the partnership signals that institutional adoption of stablecoin infrastructure is accelerating beyond crypto-native firms. Stablecoins are digital currencies pegged to a stable asset, typically the U.S. dollar, and USDC is Circle’s flagship product.

Earlier in the week, Circle announced integrations with INFINIOS in Bahrain, Munify in the Philippines, MassPay, and Nium, each of which connects USDC settlement to local payout rails in emerging markets. The Circle Payments Network, or CPN, is the infrastructure layer that makes those integrations possible. Each new integration expands the addressable market for Circle’s reserve income model, where the company earns interest on the U.S. Treasury securities that back every USDC in circulation.

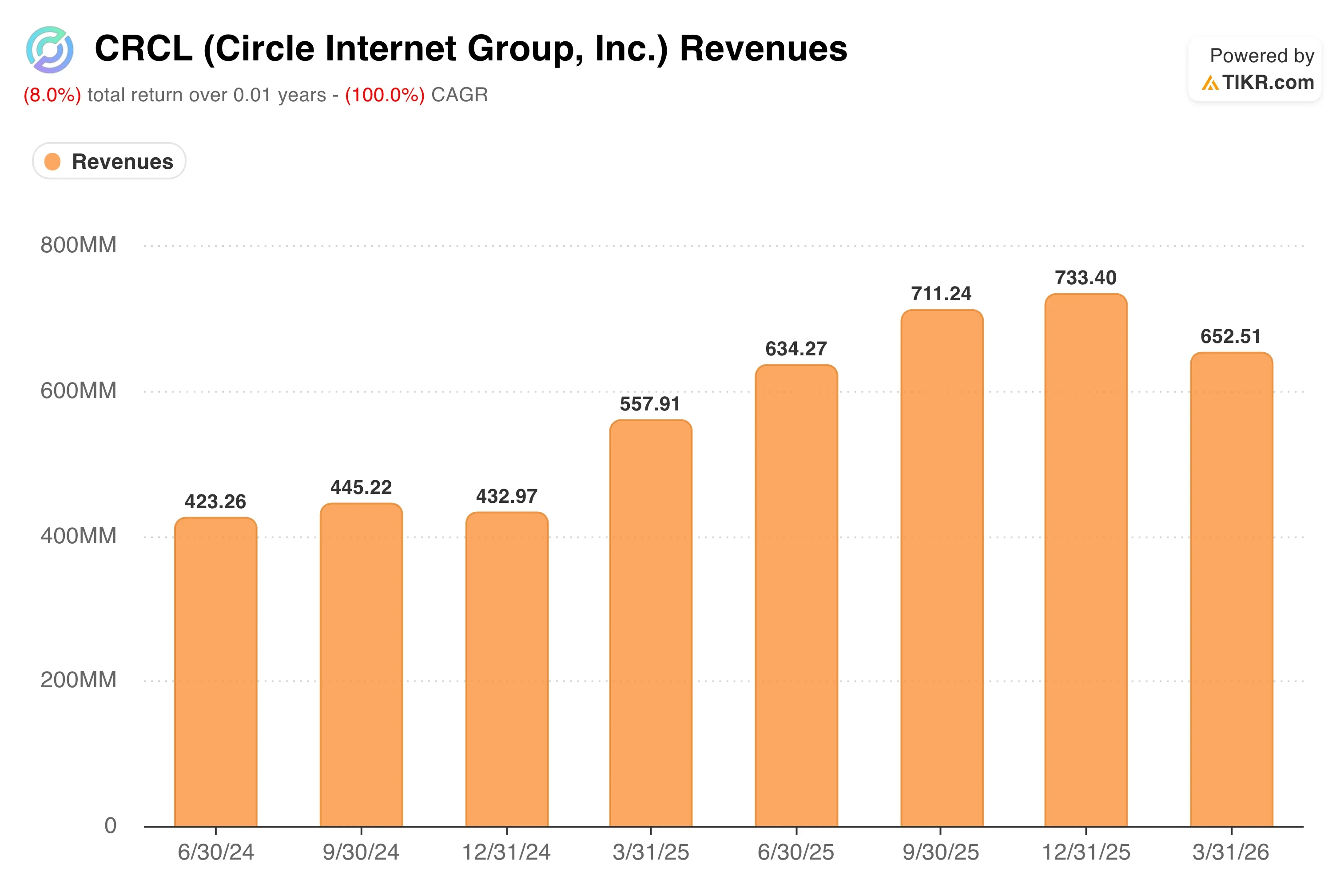

CRCL Revenues (TIKR)

CRCL Revenues (TIKR)

Circle CEO Jeremy Allaire has described USDC as a “programmable dollar” that enables instant, borderless settlement at a fraction of the cost of traditional wire transfers. Q1 results, reported May 11, showed revenue of $694 million, up 20% year over year but roughly 4% below consensus.

Net income fell 15% to $55 million, partly reflecting rising distribution costs as Circle shares reserve income with ecosystem partners. Going forward, whether the CPN expansion converts into recurring, higher-margin revenue rather than volume heavily shared with intermediaries will drive CRCL stock.

See analysts’ growth forecasts and price targets for CRCL (It’s free) >>>

Can the Stablecoin Thesis Justify Circle’s Implied Return?

CRCL Guided Valuation Model (TIKR)

CRCL Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 25.6%

- Operating Margins: 12.3%

- Exit P/E Multiple: 56.1x

Based on these inputs, the model estimates a target price of $209, implying 203.2% total upside from the current share price of $69 and a 55.3% annualized return over the next 2.5 years.

A 55.3% annualized return forecast reflects two things simultaneously: enormous upside potential and meaningful execution risk. Forward estimates that show a 25.3% two-year revenue CAGR support the credibility of the 25.6% revenue CAGR assumption, but the assumption depends on USDC supply growth as stablecoin adoption deepens across institutional and emerging-market use cases.

CRCL Guided Valuation Model (TIKR)

CRCL Guided Valuation Model (TIKR)

The 12.3% operating margin target is where the tension lives. Circle’s last-twelve-month EBIT margin is currently negative at (5.0%), and the LTM gross margin is just 8.1%. The path from today’s loss-making operating structure to 12.3% margins runs through revenue scale and a reduction in distribution costs paid to exchange and wallet partners. That is achievable but not guaranteed, particularly if USDC faces competitive pressure from bank-issued stablecoins following U.S. stablecoin legislation.

The 56.1x exit P/E multiple is elevated relative to traditional fintech valuations, but Circle is not a traditional fintech. It is closer to a digital payments infrastructure company. At the current NTM P/E of 56.1x, the model already prices the stock at the implied exit multiple, meaning earnings growth drives the entire return in the model rather than multiple expansion.

See what analysts forecast for Circle’s revenue and earnings through 2028 with TIKR >>>

Circle vs. Coinbase and Traditional Payment Networks

Circle’s most relevant public comparables are Coinbase (COIN) and traditional payment infrastructure names like PayPal (PYPL). Coinbase benefits from the same stablecoin regulatory tailwind and is the primary distribution partner for USDC. Still, it derives the majority of its revenue from trading fees rather than reserve income. Analysts forecast Coinbase’s NTM revenue growth in the mid-teens, lower than Circle’s 25% target, but Coinbase has substantially higher operating margins.

CRCL NTM Revenues vs COIN and PYPL (TIKR)

CRCL NTM Revenues vs COIN and PYPL (TIKR)

PayPal is moving into stablecoins with its own PYUSD product and has the merchant network advantage that Circle lacks. PayPal trades at roughly 14x forward earnings, a fraction of Circle’s multiple, but PayPal’s growth profile is also far lower. The comparison illustrates the valuation tension in CRCL: investors are paying for a payments infrastructure business priced like high-growth software.

The competitive moat for Circle rests on USDC’s first-mover scale and the depth of its institutional relationships. With Nomura, INFINIOS, Nium, and others joining the CPN, Circle is building network effects that are difficult for later entrants to replicate quickly. The regulatory environment also favors USDC, as Circle is the most compliant and transparent stablecoin issuer in the market, positioning it well for any U.S. stablecoin legislation that requires reserve auditing and transparency.

Read our full take on Circle’s outlook as USDC adoption expands >>>

What’s Driving CRCL Stock Going Forward?

Circle’s most important forward catalyst is U.S. stablecoin legislation, which has been advancing through Congress. A clear regulatory framework would unlock institutional adoption that legal uncertainty has deferred. Circle’s compliance infrastructure already aligns with the requirements that proposed legislation would impose, giving it a first-mover advantage if the rules crystallize.

The CPN partnership pipeline is also the clearest near-term growth driver. Each new integration expands the settlement reach of USDC without requiring Circle to build physical infrastructure. The Nomura partnership is particularly meaningful because collateral management and fund transfers are high-velocity, high-value use cases that would increase the average USDC balance in circulation and, therefore, Circle’s reserve income.

Q2 2026 results are scheduled for August 10. The key metric to watch is USDC supply growth, because Circle’s revenue model is directly tied to how much stablecoin is in circulation multiplied by the prevailing short-term interest rate. If interest rates remain elevated and USDC supply grows alongside CPN expansion, Circle’s reserve income should accelerate.

The risk that investors are pricing in is distribution cost pressure. Circle pays out a significant share of reserve income to Coinbase and other ecosystem partners as part of its USDC growth strategy. If that cost structure is not rationalized as the network scales, the path to 12.3% operating margins becomes significantly longer, and the model’s implied returns would compress materially.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Circle Internet Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRCL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRCL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CRCL stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Atlanta Mobile Lice Removal Service Surpasses 10,000 Families Treated Across 16 Georgia Locations

Metaplanet buys 5,075 Bitcoin in Q1 to become 3rd-largest treasury

Cardano’s ADA falls 1.09% to $0.1452, analysts watch $0.092 support as market sentiment weakens