Got $2,500? 1 Unstoppable Dividend Aristocrat With an Ironclad Moat to Buy

The post Got $2,500? 1 Unstoppable Dividend Aristocrat With an Ironclad Moat to Buy appeared first on 24/7 Wall St..

- Abbott Laboratories (ABT) — 54 consecutive years of dividend increases fund multi-decade retirement portfolios.

- Abbott's four-segment model offsets weakness: Medical Devices +13.2%, Diagnostics +6.1%, Nutrition -6.0%, total revenue +7.8%.

- FreeStyle Libre continuous glucose monitor generates $2.08B quarterly (+13.8%) with sticky, consumable razor-and-blade economics.

- Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Abbott Laboratories didn't make the cut. Grab the names FREE today.

Abbott Laboratories (NYSE:ABT) is a stock with characteristics suited to multi-decade ownership, because its four-segment healthcare engine, 54 consecutive years of dividend increases, and recession-resistant end markets give a retirement-focused portfolio something rare: cash compounding that does not require monitoring.

Pillar One: Durability Built Into the Business Model

Abbott’s revenue flows from four distinct segments spanning multiple geographies and therapeutic areas, and the latest quarter shows why that matters. In Q1 2026, Medical Devices delivered $5.54 billion (+13.2% YoY), Diagnostics added $2.18 billion (+6.1%), Established Pharmaceuticals grew +13.2% in emerging markets, and Nutrition shrank 6.0%. Three segments offset the weak one, and total revenue still grew 7.8% to $11.16 billion, exactly the four-headed structure that absorbs localized blows while sustaining cash flow.

The moat keeps widening. The $21 billion Exact Sciences acquisition closed March 23, 2026, adding Cologuard and Cancerguard to the diagnostics arsenal. FreeStyle Libre, the continuous glucose monitor franchise, generated $2.08 billion (+13.8% YoY) in the first quarter alone, a consumable razor-and-blade business that, as global diabetes rates climb, creates an exceptionally sticky customer relationship.

Pillar Two: Income You Can Set and Forget

Abbott just paid its 409th consecutive quarterly dividend. The quarterly payout has climbed from $0.14 in 2013 to $0.63 in early 2026, with the most recent declaration set at $0.740243 per share, payable August 17, 2026. The trailing dividend currently yields 2.76%, modest at the surface, meaningful when paired with a multi-decade compounding curve. Backing the payout: trailing twelve-month revenue of $45.1 billion, a 13.9% profit margin, and a forward P/E of 16.

Pillar Three: Why It Survives Cycles

Healthcare demand is largely non-discretionary. Glucose monitors, heart valves, lab diagnostics, and infant nutrition do not get postponed when GDP wobbles. The numbers reflect that defensive profile: a beta of 0.62, 82.67% institutional ownership, and operations across 160-plus countries. Management is guiding full-year 2026 to comparable sales growth of 6.5% to 7.5% and adjusted EPS of $5.38 to $5.58, even after absorbing $0.20 of Exact Sciences dilution.

Where It Underperforms

In low-rate, high-growth bull markets, a defensive aristocrat with a beta of 0.62 will trail high-beta technology and small caps. Abbott is also down 30.67% over the past year as the market rotated toward speculative names. That lag does not change the forever thesis. Owners of a Dividend Aristocrat are paid in compounding payouts and capital preservation, not in narrative-driven rallies, and the same low-volatility profile that caps upside in bull runs is what protects capital when the rotation reverses.

At a price of $90.53, well below the analyst target of $116.54 and the 200-day moving average of $113.41, the current setup combines a meaningful yield, a 54-year dividend-growth track record, and exposure to chronic-disease secular growth. The setup favors long-duration ownership over short-term trading.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Abbott Laboratories didn’t make the cut. Grab the names FREE today.

The post Got $2,500? 1 Unstoppable Dividend Aristocrat With an Ironclad Moat to Buy appeared first on 24/7 Wall St..

You May Also Like

BNB slips below $590 as Trump threatens to strike Iranian power plants

Bitcoin Slides Toward $59K as DXY Strengthens—Market Outlook Shifts

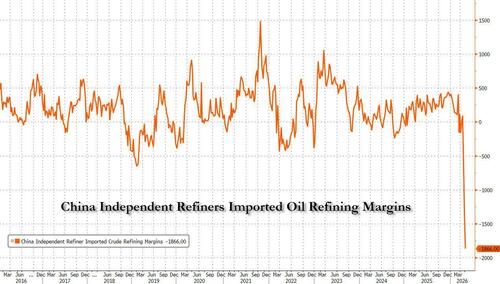

China's Refiners Slash Runs To Lowest Since 2017, As Asia Refiners Slow Purchases Of Mid-East Oil