Gold Price Prediction: Dead Money or the Buy of the Decade? Bond Market Says Watch June 17

old did not have a great week. The metal dipped roughly 5% and now trades near $4,300 per ounce. The tourists left. The momentum crowd rotated into AI stocks. Even some long‑time gold bugs started dumping their insurance at the bottom.

A few months ago, gold was the market’s favorite trade. Today it feels almost completely abandoned. It did something worse than a crash for a thesis but better for an entry. It got boring.

That is exactly when a relatively unknown analyst on X – TSCS – decided to speak up. He posted a long, detailed thread arguing that the crowd has it backwards. Gold is not dead. The bond market is breaking, a new Fed chair walks into a corner on June 17, and the selloff is the buy signal.

Let us walk through his argument, add our own take, and then give a gold price prediction for the weeks ahead.

TSCS’s Thread: Gold Is the Punchline, Bonds Are the Story

TSCS started with a confession. Gold miners are a fifth of his book. He sat through a 27% drawdown in the sector over seven weeks. Two months ago, near the bottom, he told gold bugs not to panic. Nothing since has put a scratch on his thesis.

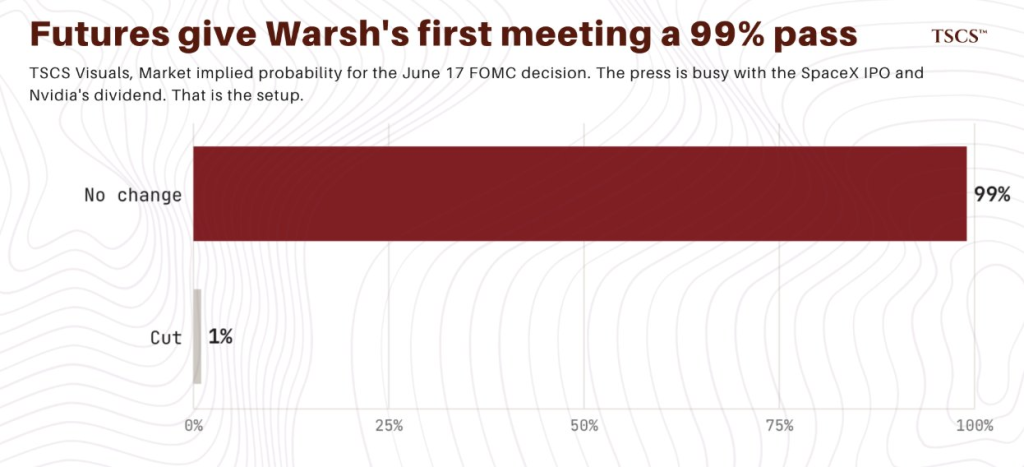

But his letter is not really about gold. Gold is the punchline. The setup is the bond market, a new Fed chair walking into a corner, and a date almost nobody is watching. In twelve days, on June 17, Kevin Warsh chairs his first meeting as head of the Federal Reserve.

Source: X/@SCapStrategist

Source: X/@SCapStrategist

The market has decided it is a non‑event. Futures put the odds of no change near 99%. The financial press is busy with the SpaceX IPO and Nvidia’s dividend. TSCS calls it the most important macro event of the year, and possibly the decision that defines the next decade.

The Fiscal Trap: Why the Fed Cannot Fight Inflation

TSCS leans on the fiscal‑dominance thesis from Lyn Alden, Russell Napier, and Luke Gromen. Once the debt is large enough, the Fed can no longer fight inflation with higher rates without making the fiscal hole deeper.

Here are the numbers. In the last fiscal year, the federal government spent $970 billion servicing its debt – more than defence, and nearly a fifth of every dollar of revenue collected. Gross federal debt sits at about 124% of GDP, against roughly 30% when Paul Volcker raised rates to nearly 20% in 1980. The country could survive that pain then. It cannot now. Close to $10 trillion of its debt rolls over in the next twelve months. Every extra point of yield feeds straight back into the deficit.

And yet the ten‑year Treasury yield broke above 4.4% a couple of weeks ago and has not come back. It sits near 4.5%, climbing on a strong jobs print and rising oil. The market suddenly prices a possible rate hike by year end instead of the cuts everyone had penciled in.

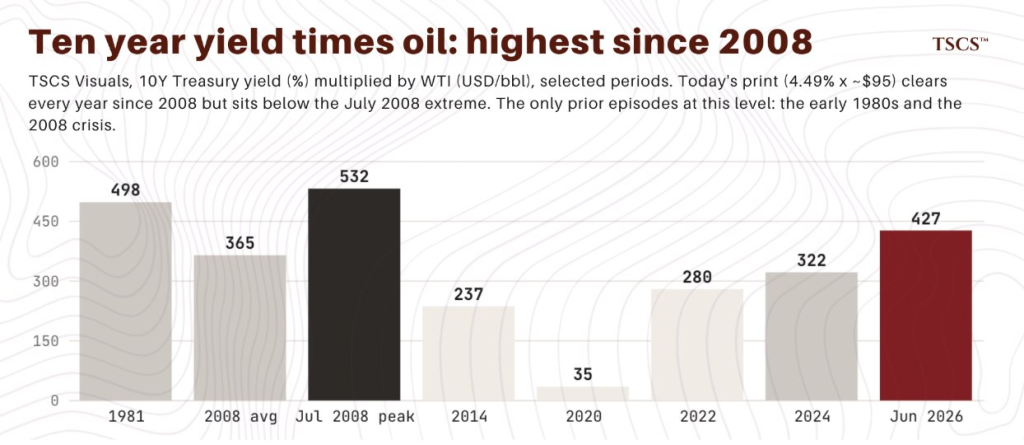

TSCS highlights a simple measure from a friend of Gromen’s: the ten‑year yield multiplied by the price of oil. Rising yields and rising oil are both poison to a heavily indebted, heavily financialised economy. That number is now at its highest since the 2008 crisis. The only other times it ran this hot were the on‑ramp to 2008 and the recessions of the early 1980s. We are back in that zone, and the S&P 500 is at an all‑time high.

Source: X/@SCapStrategist

Source: X/@SCapStrategist

The trap: you cannot have a strong dollar, a rising stock market, reshoring, and rising oil all at once in a country this indebted. Something has to give. Save the dollar by letting yields go wherever they want, and the interest bill alone bankrupts you. Save the bond market by printing money to cap yields, and you debase the currency on purpose. There is no door marked “everything is fine.”

Kevin Warsh: The Sleight of Hand

Kevin Warsh was confirmed last month by the narrowest margin for any Fed chair in modern history – 54 to 45. He inherits a central bank with inflation at a three‑year high, an oil shock pushing it higher, and a committee whose last decision split eight to four, with four members dissenting in favour of a cut.

Warsh is on the record calling for lower interest rates. He also wants to shrink the Fed’s balance sheet faster. He has called for regime change at the institution he now runs. Read those two positions again. He wants lower rates and faster quantitative tightening into an oil spike with inflation accelerating. He cannot do both cleanly.

TSCS thinks Warsh will use a sleight of hand: sell bonds at the long end (so he can say he is shrinking the balance sheet), cut rates at the short end, and lean on regulatory changes that make it easier for banks to hold Treasuries. The name for where that leads: inflation will be three and greatness will be six. You let it run while insisting you are not.

June 17 is the day the market finds out whether the new chair fights inflation or feeds it. Given the fiscal math, TSCS argues the long‑run answer writes itself.

Where Gold Fits: The Broken Real‑Yield Relationship

Almost everyone selling gold today is selling for the same reason. Real rates are rising. Hike odds are back. The oldest rule says you do not own gold when real rates rise. That rule was correct in normal times. These are not normal times.

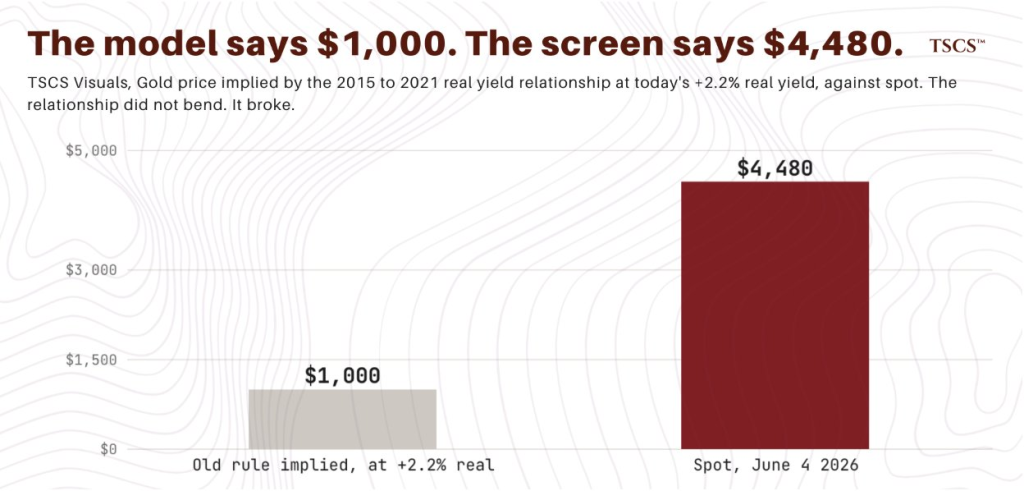

TSCS points to the chart. For a decade, the relationship was mechanical. At a real yield of plus 1.1% in 2018, gold was $1,220. At minus 1% in 2020, it was nearly $2,000. Now look at the right edge. The ten‑year real yield is about 2.2%, near the highest in fifteen years. A simple real‑yield model would have put gold near $1,000. It is $4,480. The relationship did not bend. It broke.

Source: X/@SCapStrategist

Source: X/@SCapStrategist

Rising real rates on a sovereign that cannot fund itself at these rates is the most bullish setup gold can have. A government that cannot afford its interest bill has two ways out. Default – catastrophic and wildly bullish for gold. Or print money to cap yields – also bullish for gold. There is no third door where rising real rates grind the sovereign down quietly and nothing breaks. So the very thing scaring people out of gold – rising real rates – sets up the next leg.

Central Banks as the Structural Floor

Official demand reset sharply higher after 2022, when the West froze Russia’s reserves. Central banks bought more than a thousand tonnes in 2022, 2023 and 2024, then about 863 tonnes in 2025, against a 2010‑2021 average near 470. Measured at market value, gold has now overtaken the euro as the second largest reserve asset held by central banks, behind only the dollar.

TSCS is honest about the risks. 2025 buying was down on 2024. It is concentrated in a handful of states. A good share is estimated rather than directly reported. And gold’s 2025 run also leaned on ETF and bar‑and‑coin demand. The official bid is the floor, not the only buyer.

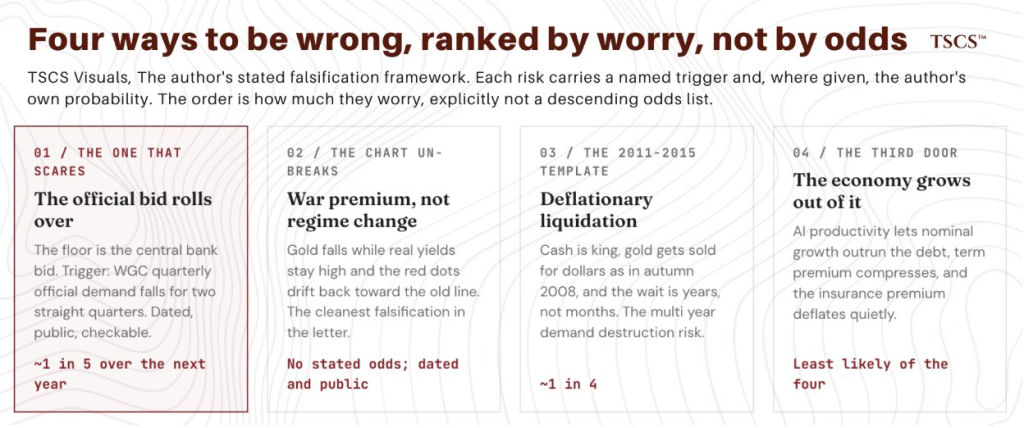

What Could Go Wrong? Four Risks

TSCS lists four ways he could be wrong. First, official demand rolls over for two straight quarters. Second, the old gold‑real‑yield relationship un‑breaks, meaning the decoupling was a war premium, not a regime change. Third, a disinflationary liquidation (1930s style) where even gold gets sold for dollars – he puts real weight on that, maybe one in four. Fourth, AI‑driven productivity grows the economy out of the trap, making gold’s insurance premium deflate quietly.

Source: X/@SCapStrategist

Source: X/@SCapStrategist

He also warns of a near‑term flush. The dollar is sitting right on a ceiling around 99.5. If Warsh comes out hawkish on June 17, the dollar breaks out, and oil spikes (some majors call Brent at $150‑$160), then both kinds of selling hit at once.

Gold and miners could take another 15‑20% hit. He puts that flush at roughly one in four over the near term. His base case is not a straight line up.

Our Take: The Logic Is Sound, But Timing Is Everything

TSCS makes a compelling macro case. The fiscal math is real. The bond market is flashing stress signals that most equity investors ignore. And the decoupling of gold from real yields is the most important data point in the entire precious metals space.

We agree with the long‑term bullish thesis for the gold price. A government that cannot afford its own interest bill has only bad options. Gold benefits from all of them.

But the near term is genuinely two‑sided. June 17 is the key date. Warsh’s tone, his dot plot, and his first press conference will set the direction for the dollar, bonds, and gold. A hawkish surprise could trigger the flush TSCS describes. A dovish lean would send gold toward $4,800 quickly.

For investors with a multi‑year horizon, the current $4,300 level offers a reasonable entry – especially for physical gold or high‑quality miners. For shorter‑term traders, waiting until after the June 17 meeting to see Warsh’s hand makes sense. The risk of a 15‑20% flush is real enough to demand patience.

Gold Price Prediction (Short‑Term and Long‑Term)

Let’s have a look at our current gold price predictions:

Short‑term (next 2‑3 weeks, into June 17): Expect range‑bound action between $4,200 and $4,500. If Warsh signals a dovish tilt (lower rates, slower QT), the gold price breaks $4,600 and heads toward $4,800. If he surprises hawkish (higher for longer, dollar breakout), gold tests $4,000 support. The most likely outcome is a bounce toward $4,500 as the market prices in fiscal dominance, but the flush risk keeps a lid on upside until Warsh speaks.

Medium‑term (3‑6 months): Once the market realises the Fed cannot fight inflation without bankrupting the country, gold resumes its uptrend. A move to $5,000 by Q4 2026 is plausible. Central bank buying and ETF inflows returning from the sidelines will provide fuel.

Long‑term (12‑18 months): If fiscal dominance fully takes hold and the US chooses debasement over default, gold could reach $5,500‑$6,000. The miners would multiply those gains. The main downside risk is the disinflationary liquidation scenario (1930s style) – but TSCS and we both view that as less likely than the inflationary path.

FAQs

For long‑term holders, yes – with a tolerance for a possible 15‑20% flush. For short‑term traders, waiting until after June 17 carries less risk.

Gold is a good long-term investment, particularly as a portfolio hedge. With central banks aggressively buying gold (absorbing an estimated 244 tons in Q1 2026) to diversify away from dollar reserves, and rising U.S. sovereign debt risks eroding confidence in traditional assets, the metal acts as a counterweight to equities and bonds

Subscribe to our YouTube channel for daily crypto updates, market insights, and expert analysis.

The post Gold Price Prediction: Dead Money or the Buy of the Decade? Bond Market Says Watch June 17 appeared first on CaptainAltcoin.

You May Also Like

Bitcoin ETFs Rout Extends To June With $1.72 Billion Net Outflows In First Week

Crypto Just Had Its Worst Week in Years — Is it a Buying Opportunity?

Worldcoin (WLD) Crashes 28% After Arthur Hayes Exits Entire Position