Dell Has More Than Tripled in 2026. At $410, Is the AI Server Re-Rating Already Over?

Key Stats for Dell Stock

- Current Price: $409.50

- Target Price (Mid): ~$530

- Street Target: ~$485

- Potential Total Return: ~30%

- Annualized IRR: ~6% / year

- Earnings Reaction: +32.76% (May 28, 2026)

- Max Drawdown: 32.64% (January 20, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Line that Reframes the Dell Story

Dell Technologies (DELL) has more than tripled this year, and the market still cannot agree on what the stock is worth. Bulls see the clearest hardware winner of the AI buildout. Bears see a low-margin box maker priced like a platform after a huge run. At $409.50, down from a 52-week high of $469.47, the stock sits between those views. The question investors keep asking is simple: after a move this big, is Dell still cheap, or is the easy money gone?

A June 2 fireside chat answered part of it. At the Bank of America Global Technology Conference, Arthur Lewis, president of Dell’s Infrastructure Solutions Group (ISG), the division that sells servers, storage, and networking gear, was blunt about the raised outlook. The new guide, he said, “is only gated by supply. The demand that we’re seeing far exceeds the supply that we have.” That reframes the bear case. The risk is not whether customers want Dell’s AI servers. It is whether Dell can ship them fast enough, and at what margin.

Why “supply-gated” Changes the Math

For most of 2026, the debate was about demand durability. Lewis moved it somewhere harder to argue with, saying Dell now has order visibility “into ’26, into ’27, into parts of ’28.” When the constraint is supply rather than demand, near-term revenue depends on execution and component access, not on winning deals.

The latest quarter backs that up. Per Dell’s fiscal Q1 2027 release on May 28, the stock jumped 32.76% the next day, its sharpest earnings reaction in years. Dell reported record revenue of $43.84 billion, with AI-optimized server revenue up 757% to $16.13 billion. Management then raised full-year revenue guidance to $165 billion to $169 billion and now expects around $60 billion of AI server revenue this year. That was not just enthusiasm. It was a repricing of how big Dell’s revenue base could get.

See historical and forward estimates for Dell stock (It’s free!) >>>

The Part that is Quietly About Margins

The bear worry has always been that AI servers carry thinner margins than Dell’s traditional products. Lewis pushed back, and storage is where it lands. He said Dell’s own intellectual property storage has been “growing on a demand basis well ahead of the market for 5 consecutive quarters,” and that “Dell IP storage is more valuable than partner IP.”

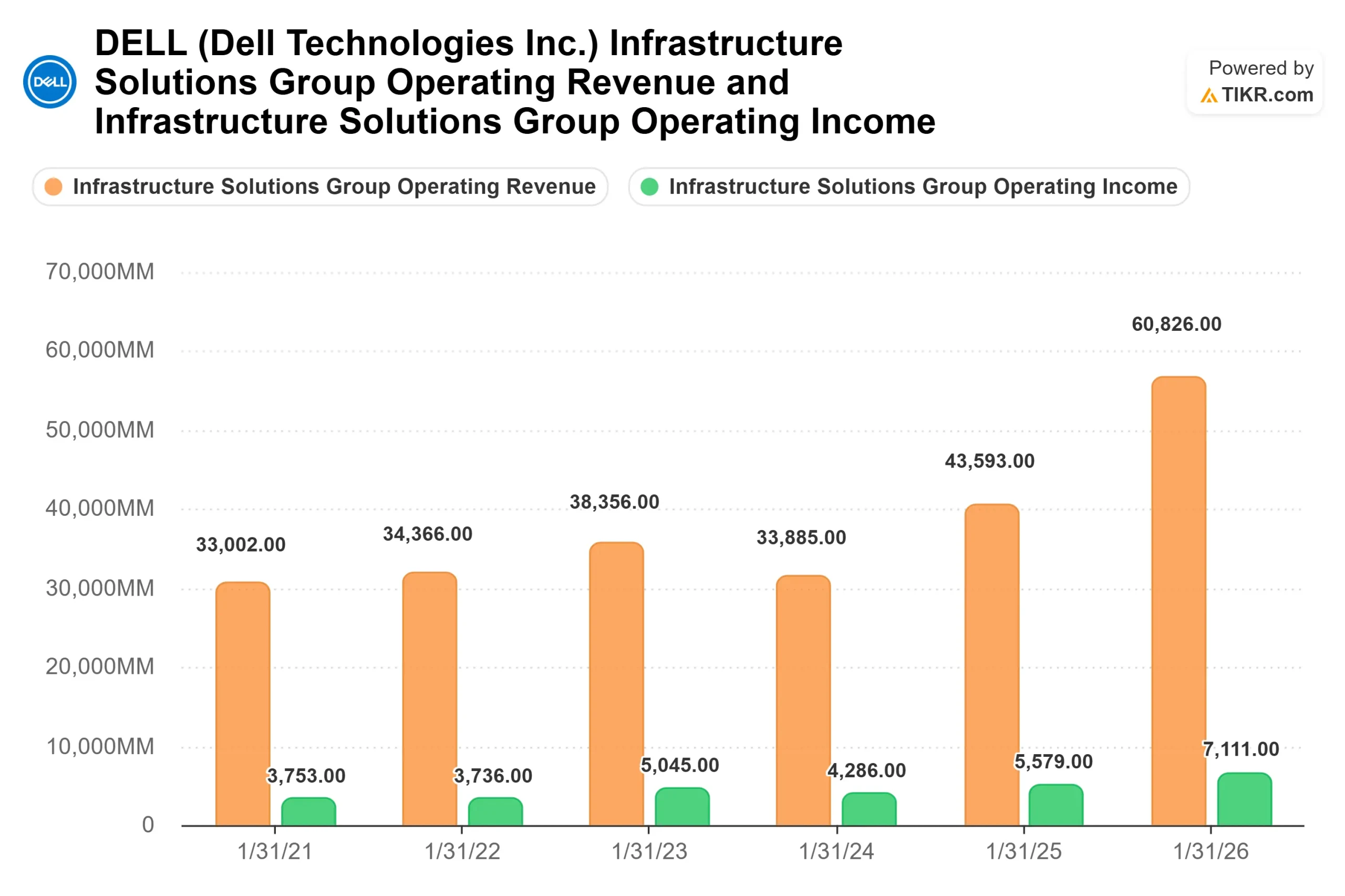

That connects to a product investors can track. Dell’s new PowerStore Elite storage platform becomes globally available in July 2026. Storage is a higher margin than servers, and every AI server shipped is a chance to attach it. Per Dell’s reported quarter, ISG operating margin held at 10.5% even with the heavy AI mix, up from 9.7% a year earlier. The attach strategy and scale are offsetting thinner server economics, not being buried by them.

There is a second tailwind. As AI shifts from models that think to agents that act, more workloads run on standard CPUs, because agentic tasks are “a serial sequential process that requires a CPU,” Lewis said. That helped traditional servers and networking revenue grow 92% in the quarter. The legacy business is not fading. Agentic AI is feeding it.

How Dell stacks up against peers

Here is the tension the run created. Even now, Dell trades cheaper than most hardware peers. Its next twelve months (NTM) price-to-earnings (P/E) multiple sits at 22.19x, against a peer median of 14.42x. But that median is dragged down by slower names. On EV/EBITDA, which weighs total value against core earnings, Western Digital trades at 32.30x and Seagate at 34.06x, both far above Dell’s 15.03x, while Lenovo sits at 8.01x.

So the premium-or-discount question has no clean answer, and that is the point. Dell is neither the cheapest box in the group nor the most expensive, yet it grows faster than almost all of them. For a company guiding to roughly $60 billion in AI server revenue this year, a 22x forward multiple is a bet that the growth is real and the margins hold as volume scales. That is exactly where bulls and bears still split.

Dell NTM Price / Normalized Earnings (P/E) (TIKR)

Dell NTM Price / Normalized Earnings (P/E) (TIKR)  Dell ISG Operating Revenue & Income (TIKR)

Dell ISG Operating Revenue & Income (TIKR)

See how Dell performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $409.50

- Target Price (Mid): ~$530

- Potential Total Return: ~30%

- Annualized IRR: ~6% / year

Dell Advanced Valuation Model (TIKR)

Dell Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Dell stock (It’s free!) >>>

The mid case is used here because it assumes real deceleration from current growth, and the reasonable base case as the AI cycle matures. The target rests on two revenue CAGR drivers: AI server revenue scaling toward the roughly $60 billion run rate, and higher-value storage and services attached around those systems. The margin driver is mixed, with Dell IP storage growing faster than lower-margin servers. The main risk is that the same mix turning against Dell if servers grow while attach lags, or if memory costs squeeze pricing.

The upside: if backlog conversion and attach hold, the high case points to roughly 80% total return, about 7% annually.

The downside: if growth slows faster than modeled, the low case lands near 11% total return, just over 1% a year.

Conclusion

The next read on this thesis is Dell’s fiscal Q2 2027 report, expected in late August 2026. Management guided to around $44 billion to $45 billion in revenue and about $4.80 in adjusted earnings per share. The number that matters most is ISG’s operating margin. Good looks like a margin at or above the 10.5% Dell just posted, while AI server revenue keeps scaling. Bad looks like margin slipping as AI mix climbs, which hands the bears their case. Street sentiment is constructive heading in, with 14 Buys, 5 Outperforms, 8 Holds, 1 No Opinion, 1 Underperform, and 1 Sell. The supply is spoken for. The open question is what it earns on the way out the door.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Dell?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Dell, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dell alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Dell on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Adoption Leads Traders to Snorter Token

Harvard scholar: the data-center backlash is just getting started

Goatseus Maximus (GOAT) Price Prediction 2026, 2027-2030