GE Vernova Rose 6% Today. Why Its Power Backlog Could Drive More Upside in 2026

Key Stats for GEV Stock

- Today’s Performance: 6%

- 52-Week Range: $479 to $1,182

- Valuation Model Target Price: Around $1,210

- Implied Upside: Around 9%

Analyze your favorite stocks like GE Vernova with TIKR (It’s free) >>>

What Happened?

GE Vernova Inc. stock rose about 6% today, trading near $1,110 per share as investors continued to favor companies tied to rising power demand, grid investment, and AI data center infrastructure. Shares stayed near their 52-week high of about $1,180, showing that investors are still willing to pay a premium for businesses positioned around the power shortage theme.

The stock rose today because fresh analyst support and recent company commentary reinforced the same story: GE Vernova’s large backlog could translate into years of higher revenue, better margins, and stronger free cash flow. Bernstein recently started coverage with an Outperform rating and a price target of around $1,210, close to TIKR’s Street target price and valuation model target. The call helped support the stock today because it reinforced the same thesis investors are paying for: GE Vernova’s backlog, grid exposure, and margin expansion could keep earnings moving higher into 2026.

Peer activity also supported the broader power equipment story. Siemens Energy recently reported a record order backlog of €154 billion and revenue growth of 9%, while Mitsubishi Heavy Industries remains a major gas turbine competitor as utilities and industrial customers race to secure power capacity. That matters for GE Vernova because the strongest power equipment names are seeing the same demand pattern: gas turbines, grid equipment, transformers, and electrical infrastructure are being booked years in advance.

At Bernstein’s Strategic Decisions Conference, GE Vernova CEO Scott Strazik highlighted the company’s long-cycle demand strength, saying backlog has grown from $116 billion at spin to $163 billion, including $87 billion in services backlog and $76 billion in equipment backlog. Strazik said GE Vernova generates 25% of the world’s electricity each day and has 100 gigawatts of gas equipment on contract, while electrification remains its fastest-growing business, with backlog rising from $9 billion at the end of 2022 to $42 billion at the end of Q1 2026. Data centers represent about 20% to 25% of backlog today, but Strazik pushed back on the idea that growth is only tied to a short AI cycle, saying, “the opportunity is significant and is going to go for a very long time.”

Recent financial results also supported the move. GE Vernova reported Q1 revenue of $9.3 billion, up 16% year over year, adjusted EBITDA of $0.9 billion, and adjusted EBITDA margin of 9.6%, while EPS reached $17.44, helped by a one-time gain tied to the Prolec GE acquisition. The company also raised its 2026 outlook to revenue of $44.5 billion to $45.5 billion, adjusted EBITDA margin of 12% to 14%, and free cash flow of $6.5 billion to $7.5 billion, giving investors more confidence that stronger demand can translate into cash flow and capital returns.

GE Vernova Guided Valuation Model

GE Vernova Guided Valuation Model

Value GE Vernova instantly (Free with TIKR) >>>

Is GE Vernova Fairly Valued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): Around 15%

- Operating Margins: Around 12%

- Exit P/E Multiple: Around 47x

GE Vernova looks closer to fairly valued than deeply undervalued because the model estimates a target price of around $1,210, implying around 9% total upside.

The 15% revenue growth assumption is mainly supported by backlog conversion in Power and Electrification, where gas turbines, grid equipment, transformers, and power conversion systems are seeing strong demand from utilities, industrial customers, and AI data centers.

The 12% operating margin assumption depends on GE Vernova turning more equipment orders into higher-margin services revenue, while also improving profitability in Electrification and limiting the drag from Wind.

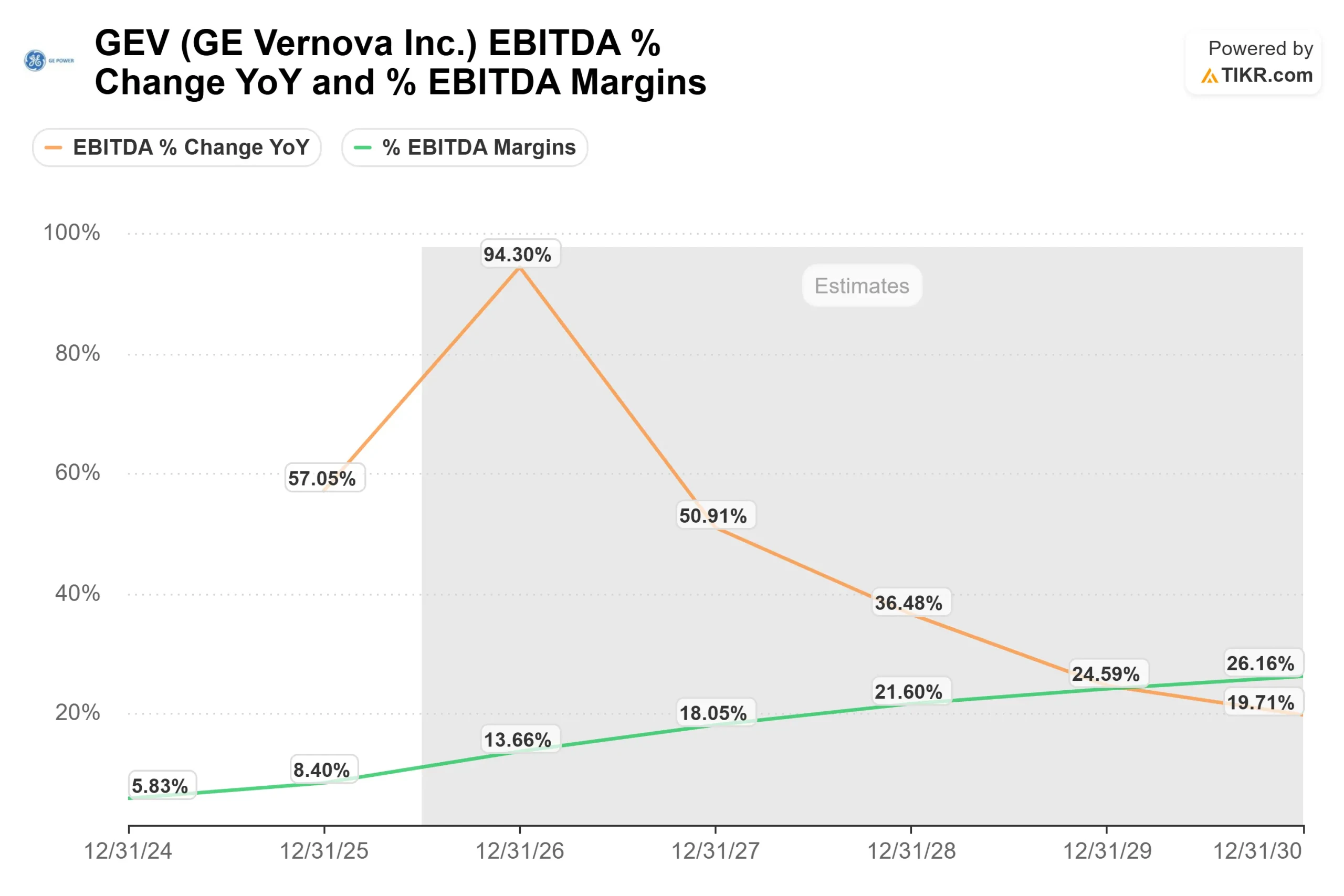

GE Vernova EBITDA Margins and Analyst Profitability Estimates Over Five Years

GE Vernova EBITDA Margins and Analyst Profitability Estimates Over Five Years

See analysts’ growth forecasts and price targets for GE Vernova (It’s free) >>>

The EBITDA chart supports that margin story, showing EBITDA margins rising from about 6% in 2024 to an estimated 14% in 2026, with analysts expecting margins to keep improving through 2030.

GE Vernova competes with global power equipment players such as Siemens Energy and Mitsubishi Heavy Industries, but its $163 billion backlog, 100 gigawatts of gas equipment on contract, and fast-growing electrification business give it strong visibility in a market where customers are trying to secure power capacity years in advance.

At current levels, GE Vernova appears fairly valued, with future returns likely driven by backlog conversion, margin expansion, and free cash flow growth rather than another major valuation reset.

How Much Upside Does GE Vernova Stock Have From Here?

Investors can estimate GE Vernova’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value GE Vernova in under 60 seconds with TIKR (It’s free) >>>

You May Also Like

The yoghurt fight thickens as Danone sues Chobani over protein labels

Upbit Halts TAIKO Deposits and Withdrawals Amid Network Issue

Bithumb Temporarily Halts TAIKO Deposits and Withdrawals Due to Mainnet Issue